Call Us & Get Prequalified For Your Loan

First Capital Business Finance

First Capital

At First Capital, we understand that businesses face diverse challenges, and credit history should not be a barrier to growth. Our Bad Credit Business Loans are designed to provide accessible and practical financing solutions, empowering businesses to thrive despite credit constraints. Whether you’re a startup, a small business, or an established enterprise with a less-than-perfect credit history, First Capital is committed to supporting your financial needs. Explore our range of tailored financing options and embark on a journey towards business success, unencumbered by credit challenges.

What Sets First Capital Apart:

Understanding and Empathy: We recognize that businesses encounter various financial situations, and we approach each case with empathy and a commitment to finding viable solutions.

Transparent Terms: At First Capital, transparency is paramount. We lay out clear terms, ensuring that businesses have a complete understanding of the costs, repayment structures, and benefits associated with our bad credit business loans.

Diverse Financing Options: Choose from a range of financing products that cater specifically to businesses with bad credit. From term loans to lines of credit, our diverse options provide flexibility to address unique financial needs.

Quick and Simple Application Process: We understand that time is of the essence. Our streamlined application process ensures businesses receive prompt decisions, allowing them to access the funds they need efficiently.

Financial Guidance: Beyond providing loans, we offer valuable financial guidance. Explore tips on improving credit scores, making strategic financial decisions, and planning for a more stable financial future.

We firmly believe that a less-than-perfect credit history shouldn’t hinder your entrepreneurial dreams. Our Bad Credit Business Loans are designed to empower businesses like yours with the financial support needed to thrive and grow, regardless of credit challenges.

At First Capital Business Finance, we offer bad credit business loans that can give you access to working capital that will help you grow your business. We know that a bad credit score can make other lenders turn you away, but we’ll work to find the right business loan for you even if you have bad credit, and get you the best deal. We have programs that DO NOT require a minimum credit score. That’s right, even if your credit score is under 500 we have available loan programs for you!

We have financing specialists on hand to help you find a financing arrangement for all types of business equipment, including commercial trucks and construction, office or heavy manufacturing equipment. We can even finance used equipment. We have financing and business loans for startups and existing businesses with both good and bad credit. Our terms range from 12 to 72 months, allowing you to customize financing to your business situation.

If you’re not deterred by the associated risks and you’ve chosen to proceed with obtaining a loan despite less-than-ideal credit, let’s delve into the reasons why you should contemplate higher-cost financing.

A low credit score can pose challenges when it comes to borrowing money. As a small business proprietor, there are instances when you require swift access to funds, whether it’s for covering rent or employee salaries. Additionally, there are situations where you might desire to upgrade your storefront or embark on expansion plans, but find yourself lacking the necessary cash reserves.

Arguably the most crucial motive for securing funding for your business is the necessity to sustain its operations. Nonetheless, there are compelling reasons to seek additional working capital, even when it entails greater expenses.

No-credit-check business loans offer a practical solution for businesses seeking financing without the scrutiny of a credit check.

Perhaps your credit score falls on the lower side, making you uncertain about loan eligibility or other financing options.

In most cases, several business loan categories exist that bypass the need for credit checks. These include invoice factoring, payment processor loans, and merchant cash advances. We can help compare various choices for credit-free business loans and gain insights on selecting the most suitable funding solution to meet your specific requirements.

Conversely, you might boast an excellent credit score and wish to avoid additional inquiries that could impact your credit report. Regardless of your motive, numerous small business loans are available without the need for a credit check, including some offering same-day approval.

We offer both lines of credit and loans that can give you access to much-needed working capital, too. If you are having a cash flow crunch, we can help. Our application process is simple and quick, with same- or next-day approvals possible. With our capital loan program, funding can happen in as little as five days so that you can meet immediate business needs. Our financial consultants have extensive knowledge about underwriting criteria, and they will work to guide you through the application process.

First Capital Business Finance has repayment terms ranging from three to 24 months. Business Loan amounts are available from $5,000 to $2 million, so you can get the capital you need even if your credit isn’t where it should be. We don’t require you to have a credit card processing agreement or to put real estate up as collateral. We offer generous and flexible business loans for bad credit with just these minimum qualifications:

In certain scenarios, opting for a bad credit business loan can be a prudent choice, particularly within industries grappling with hyperinflation. Take, for instance, sectors like construction, trucking, and hospitality, where profit margins are notably high or on the rise. In such cases, the decision to secure financing at slightly elevated rates becomes more justifiable.

Consider this: If a $10,000 investment promises a $45,000 return, what value would you place on that initial $10,000? To put it differently, if your construction project demands a $10,000 piece of equipment to complete a job that guarantees a $45,000 profit, would you consider financing it if you lacked the cash upfront? Most often, the answer would lean toward a resounding “yes.” The lingering question is the precise worth of that capital.

Now, this isn’t to suggest that business owners should dismiss the importance of financing costs entirely—far from it. They should, indeed, scrutinize these costs with diligence. However, in dire situations, this assessment should be conducted devoid of emotional influence and grounded in a judicious analysis of profit and loss.

As we mentioned earlier, it’s important to acknowledge that bad credit business loans typically carry higher financing expenses. Lenders assume greater risk and, consequently, attach a premium to the capital extended to businesses. When entrepreneurs perceive capital as commodities they procure, they’re better poised to make sound business choices.

The crux here is that many business proprietors will encounter temporarily heightened financing costs. If your credit history is less than stellar, brace yourself for potential “sticker shock” in terms of financing expenses. However, it’s imperative not to allow this initial surprise to escalate into emotional distress. Conduct your due diligence, explore various options, and determine whether the somewhat higher cost of financing aligns with your overall business objectives.

At First Capital Business Finance, we don’t just provide loans; we foster partnerships for success. Our dedicated team is committed to supporting your business journey:

Don’t let past credit challenges define your business’s future. Embrace the possibilities with our Bad Credit Business Loans. Contact us today to discuss your business goals, explore financing options, and embark on a journey toward growth and success.

Empower your business to thrive, no matter the credit history. Choose First Capital Business Finance for Bad Credit Business Loans that turn challenges into triumphs.

Take the first step toward financial resilience and growth with First Capital’s Bad Credit Business Loans. Our team is dedicated to supporting businesses like yours, ensuring that credit challenges do not hinder your path to success. Apply today and experience the difference of a financial partner that prioritizes your business’s potential over past credit history. Your journey to financial empowerment begins here with First Capital.

First Capital

It’s challenging to be a small business owner in 2020. The COVID-19 pandemic forced institutional and economic change beyond personal health mandates. The spread of the illness required governments to shut down borders and businesses, requiring self-quarantine and isolation. While the drastic and necessary measures curbed the increasing numbers of infected, the disease has severely compromised many small businesses.

We, here at First Capital Business Finance, understand the pain of the millions of small business owners around the country. While governments currently lift many restrictions on forced closures, these businesses are still struggling with new regulations, like social distancing and mask mandates. Despite the necessity of such measures, there is no denying the harm being done to small businesses nationally and globally, so what can you do to improve your cash flow and survivability during these harsh economic times? You can apply for a business loan.

The most significant problem for business owners during the current pandemic is the loss of cash flows. As governments called for shutdowns, companies were essentially stripped of cash. The loss of money leads to debt, which can result in more severe problems, like closure.

Applying and securing a business loan through us can help resolve your current cash flow issues, allowing you to stay current on bills and avoid using other payment methods, like high-interest credit cards. While credit cards may seem like a viable option for the short term, if the debt is carried over long periods, you pay much more than the initial bill.

The current health crisis is forcing every industry and enterprise to reconsider strategies and operations. While small businesses have taken the largest financial hit, even large, well-established organizations are reporting significant losses over the last quarter, with further losses expected on year-end reports. Adapting to the new normal is a must, but, to evolve or change with the times, companies must find the capital necessary to breathe and survive.

Business loans offer a saving grace in these uncertain times, especially as reopening begins. Small businesses have no doubt felt the struggle more than most, with closures in the hundreds of thousands. A loan from us can help you stay afloat until your revenue streams reignite, and our financing can help in several ways.

If you survived mandated closure without building debt, you’d most likely need help purchasing equipment and supplies for reopening. With limited, if any, cash flows or income over the last several months, many business owners are turning to personal accounts to fund their reopening, which is risky.

Reopening in the age of COVID-19 means adhering to local sanitation and social distancing guidelines. You will inevitably need to alter your operations for habitual cleaning regimens and reduced capacities. A loan can help you purchase necessary cleaning equipment, signage, and other essentials

First Capital Business Finance is a trusted alternative lender, and since 2009, we have helped businesses like yours meet their cash flow needs. Serving small and middle-market enterprises, we provide industry-leading support through highly trained representatives, and we offer several loans and financing options for all your business needs.

While conventional bank loans require invasive and lengthy approval processes, our company aims to secure your funding as quickly as possible. We understand that during the current economic slowdown and health crisis, time is of the essence. When applying for a loan with one of our experienced representatives, you can receive approval in as little as two days with funding in five.

While you have no doubt read comments like the above from any alternative lenders, we take pride in our transparency and reputation. Don’t just take our word for our work. You can review our client testimonials to learn how our efforts helped several business owners like you handle their cash flow demands.

While the application process for any of our loans is straightforward, it is necessary to consider your business needs and select the option that best suits your current demand. Every loan type will come with specifics regarding repayment, term limits, and interest rates. You will also need to understand any restrictions that may be tied to the spending of the loan funds. Beyond researching the types of loans available, it is crucial to understand the eligibility requirements of each financing option.

While researching available loans may seem overwhelming, do not fret. Our experienced representatives are here to help you find the best solution for your business needs. They will walk you through the typical eligibility requirements and specifications of our loan programs.

Reduced risk is often tied to longevity, which is why traditional bank loans tend only to deal with well-established businesses. Our institution, alternatively, caters to the often underserved market of new and small business owners. First Capital Business Finance offers loan programs aimed at businesses one year or younger.

Serving such young businesses is a potential risk for us. Still, we trust that industries are better served with a variety of competition. Nothing makes us happier than helping the underserved entrepreneurs find affordable financing options to grow and thrive through times like these.

One of the primary contributors to loan approval for small businesses, regardless of credit score, is annual revenue and profitability. We cannot approve a loan if there is nothing to secure our interest. Your company’s profitability and revenue help to determine our risk and the likelihood of repayment. Even for borrowers with bad credit, you can still typically count on a loan offer of between 8% and 15% of your business’s annual gross revenue. That threshold provides enough security for most alternative lenders, including us.

Profitability during the current crisis and economic slowdown is not likely for many businesses, but the great news is that it does not count you out for loan approval. While demonstrating some profitability is always a good indicator of a successful business, most lenders understand the struggles of the current marketplace. Even without a pandemic, profitability only plays a partial role in loan approval, with the majority of lenders preferring annual revenue measures.

While current profitability may not be a significant concern among lenders at the moment, most will want to study your cash flows. Again, the current pandemic will contribute to the weight lenders place on this data. Still, the ability to manage cash flow is a strong indicator of the reliability of the applicant.

Cash flows, after all, demonstrate the viability of a business and its ability to meet current financial obligations. While leeway is expected amidst the current economic climate, historical data will still serve as a valuable insight to lenders.

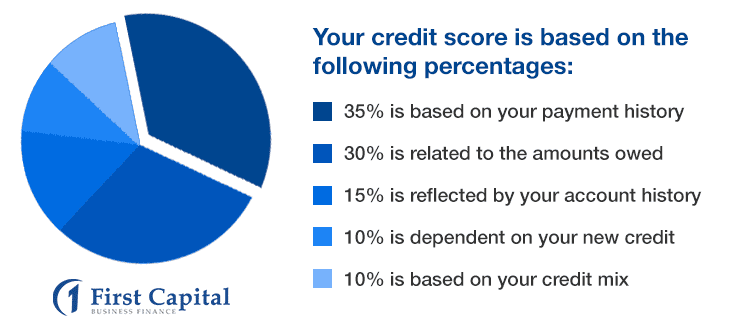

While small business owners understand the credit history of the business is investigated before loan approval, many are shocked that their personal credit history may be called into question as well. The primary indicator of overall risk to a lender is the credit score, and without a complete financial picture, it is nearly impossible to approve financing.

A credit score is often broken down into the five Cs: character, capital, capacity, conditions, and collateral. In essence, the credit score determines your reliability as a borrower by weighing your overall history.

While it may seem unfair to review personal credit history to secure a business loan, it’s necessary to consider the age of the business. A relatively young company will not have a suitable history to determine creditworthiness, especially when asking for a substantial loan.

Keep in mind that a low or bad credit score does not rule your application out, especially when working with alternative lenders like us. While you may have a hard time securing a conventional loan, we are here to service borrowers that may not fit the mold or scrutiny of traditional banks.

Conventional lenders, like credit unions and banks, require significant documentation and have stringent eligibility requirements and policies regarding loan applicants and approval. These institutions are not designed with the startup or small business in mind. Smaller enterprises often require quick turnarounds and may not have the necessary financial history needed for approval with traditional lenders.

Working with an alternative lender, like us, means less documentation, quick access to funds, fewer restrictions, and flexible terms for all credit types. By offering tailored solutions for your loan needs, we can provide various lending options, including businesses and business owners with low or bad credit.

Too many business owners assume that bad credit loans come with a range of negative caveats that will leave them worse off than before, but that is not always accurate. Indeed, predatory lenders exist even for businesses, but when working with a reputable lender, like us, you can rest assured that you’ll be better off than before.

We want to help our clients through the current COVID-19 crises, ensuring that all approved applicants walk away from the table with loan terms that are favorable and realistic. No business owner should have to risk everything to keep their dream alive. Let our skilled representatives walk you through several of the bad credit loan options available.

Among the most popular bad or low credit loans is the short-term loan. These loans offer a lump sum amount for a fixed period, typically less than a year. The payments are made according to a pre-determined payment schedule and include both the principal and interest. These loans are often based on historical financial data, but lenders may need to make exceptions based on the current crisis.

If your credit score is a concern for you, but you have consistent credit or debit card sales, you should consider a merchant cash advance. These advances offer a lump-sum against a percentage of future merchant account transactions.

While the approval process for these loans is straightforward, many businesses may not find the interest rates favorable. Therefore, before selecting this loan option, consider the costs over the life of the loan.

If you are not sure how much you need from a loan, or you are expecting future costs, then you may want to apply for a business line of credit. Lines of credit are similar to credit cards in that the business is approved for a set amount, and they can borrow against that amount, only paying interest on the portion they borrow. Therefore, the short-term business line of credit is useful in times of uncertainty.

As you begin reopening your locations, you will likely come across cash flow needs, but as the health crisis has hindered your revenue, you may need working capital. Unlike other loan types, working capital loans cannot be used for long-term assets. Instead, these loans help finance day-to-day operations, like inventory, wages, and other routine expenses. We currently offer loans of up to $500,000 to qualifying businesses, allowing you to re-establish operations after the pandemic slowdown.

Collateralized or secured business loans require invoices, equipment, or other assets to secure financing. While not always needed, when you have bad credit, providing collateral reduces the risk of the lender. However, any time collateral is used, you risk losing the asset if you cannot pay back the loan, making this loan form too risky for many business owners. Talk with one of our representatives to discuss your loan options.

Traditional or conventional lenders will have a hard time approving a loan for a business or business owner with a score of less than 650 to 700, especially if that business is less than a year old. However, as we are an alternative lender, you can find loan programs even as a new enterprise or an owner with a credit rating below 550.

The reason we can offer loan approval without adequate credit is that we allow for alternative loan options, like factoring. Therefore, while the standard benchmarks for loan approval may be too great at a bank or credit union, we can find a solution.

Testimonials

What Our Customers Say

As an alternative lender, we have experience working with small and medium-sized businesses with all types of credit histories. We understand the struggle of operational stability, especially as the economy ebbs with the current health concerns. However, even before the pandemic and government shutdowns, we helped businesses like yours secure the loans they needed to survive and thrive. We were able to help these businesses, even those with less than perfect credit, by offering unique and flexible programs.

Accounts receivable or invoice financing is a loan secured with unpaid invoices. Some lenders, like us, are willing to work with qualifying clients, advancing a percentage of existing invoices and allowing for a more straightforward approval process. However, keep in mind that these advances, a form of factoring, still accrue interest over the loan term.

Like invoice financing, equipment financing is a way of securing the loan with collateral and reducing the lender’s risk. The unique aspect of an equipment loan is that the equipment can act as the collateral. While risky because a default on the loan means repossession of the equipment, your personal assets are protected.

Aside from using invoices or new equipment, you can improve your odds of approval by offering some other form of collateral. Unfortunately, using collateral, while beneficial to the lender because of reduced risk, is riskier for the borrower. Personal assets used as collateral sit in a sort of limbo of ownership until the loan is repaid.

While not a common practice for business loans, some lenders may approve the use of a co-signer. The co-signer is an individual with a favorable credit rating and can take over payments on the loan if the primary is unable.

Taking on a business loan, especially with the current level of economic uncertainty, is risky. Still, for many small and struggling businesses, a loan is the only way to return to some form of operational normalcy after the mandatory closures and newly imposed restrictions. However, while you may need a loan to carry you through the next several months through the various phases of reopening, it is crucial that you not rush into a decision or commitment without first making several considerations.

As there are various loan types, there are different fees and costs associated with each loan program. You will want to talk with one of our representatives to determine any expenses beyond the principal. While we do our best to remain transparent, our loans are customized to suit your business needs, and as with any personalized service, the terms will be specific to your business.

The loan term is the time until full repayment, including principal and interest. We specialize in both short-term and mid-term loans. A short-term option offers terms between one and three years, whereas a mid-term repayment loan provides between two and five years for repayment.

Beyond the term, you will want to look at the limits of the loan. Most programs offer a maximum loan amount. If the loan limit does not provide enough funds, you may need to look for alternative or creative financing options. However, it is often better to find ways to reduce the required amount by cutting costs.

Interest rates are an undeniable certainty of loans, but the rate is often dependent on the overall risk to the lender. Applying for a large sum over a short-term with poor credit will likely require a higher rate of interest because the risk to the lender is more significant. However, several factors play into the rate, and one of our representatives will be happy to go over how our rates are calculated.

Before choosing a loan, make sure that you understand the level of interest you will pay. Also, consider how repayment may affect the amount of interest owed. For instance, early repayment can lower your financial obligation, but that depends on the specific loan.

Before agreeing or applying for a business loan, consider your current financial obligations. Are you already carrying a significant amount of debt, or do you already struggle to pay your business obligations, even when operating as normal? If so, taking on more financial commitments could be a mistake. One of our representatives can help you decide if a business loan is right for you.

While the COVID-19 pandemic and economic slowdown have undoubtedly affected businesses, the world and country are beginning to adapt. Your business does not need to struggle. Apply for a First Capital Business Finance loan to make reopening a success.

First Capital Business Finance is committed to helping you meet your cash flow needs to grow your business. We serve small and middle market businesses and large corporations with range of loan and financing options for bad credit

Copyright © 2024 First Capital Business Finance, All Rights Reserved

Same Day Loan Approval