Cannabusiness is the new buzzword (excuse the pun) for businesses that provide legalized marijuana for those who wish to inhale. For cancer patients, marijuana has been shown to dramatically lessen the effects of chemotherapy. Nausea and vomiting are some of the very real symptoms that accompany the use of chemical treatments used in routine cancer therapy. Around the country in at least thirteen states, medical marijuana clinics are now open and advertising for business to provide cancer sufferers relief from their treatment side effects

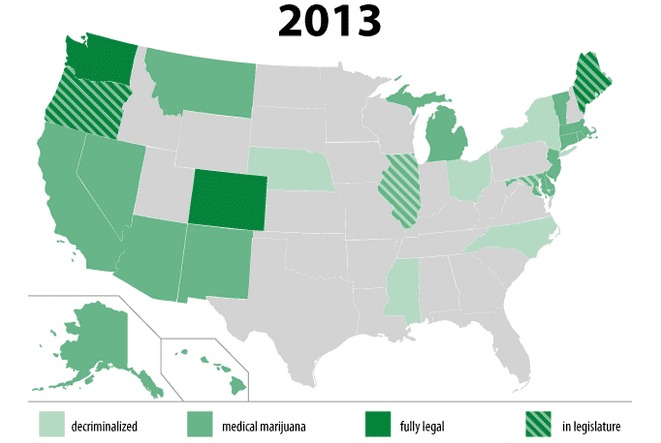

And while a few states have now legalized recreational marijuana use, many more states are considering its place for medical purposes. The burgeoning “buzz biz” has moved the federal government to ease restrictions on banks providing loans for these unique and “forbidden until now” service providers. It is obvious that marijuana’s often infamous past history had made reputable loan institutions run the other way when approached by any cannabusiness that majored in serving the medical community with their, shall we say,” leafy but shady” product line. But all that has changed as Colorado, California, and 18 other progressive states have made not only medical marijuana legal but also its recreational side as well. And as the states have loosened up, so have the strict federal laws that have governed those who have wanted to make business loans to the rapidly expanding cannabusiness.

In February of 2014, the Obama administration announced that it would “move from the shadows the historically covert financial operations of marijuana businesses,” which is to say that banks could now actually profit themselves from granting loans to cannabusinesses that offer medical marijuana as their chief income source. Oddly, while the federal government is easing loan restrictions on “Mary Jane” providers, it is still a federal offense to produce, possess or sell it.

In February of 2014, the Obama administration announced that it would “move from the shadows the historically covert financial operations of marijuana businesses,” which is to say that banks could now actually profit themselves from granting loans to cannabusinesses that offer medical marijuana as their chief income source. Oddly, while the federal government is easing loan restrictions on “Mary Jane” providers, it is still a federal offense to produce, possess or sell it.

This continues to make some traditional loan providers uneasy. One of the causes of uneasiness regarding the issue of loaning to a cannabusiness is that loan providers must give information to Washington should they suspect the weed growing business is not presenting itself truthfully. Even should the lender follow all the rules, getting pulled into an investigation could be potentially damaging to its reputation. These include civil money penalties, fines, cease-and-desist orders, or withdrawal of FDIC insurance. This could occur regardless of the medical usage of which the weed could be used. So in fact, traditional sources of capital business loans for marijuana providers, even for medical usage only, may limit cannabusinesses to more open-minded sources of financial help.

Many banks that lobby Washington is asking for legislative action from Congress to clear up murky areas of the Obama initiative. One administration’s loosening of fiscal policy could be another administration’s top priority to tighten causing total chaos among retailers. But as more and more states move to look favorably upon medical marijuana usage as legal, it is almost for certain that the federal government will move in the legal sense to normalize it for medical purposes, if not also recreationally.

One of the reasons that this new legitimized way to make a living is attracting many new entrepreneurs to the cannabusiness phenomenon is that it has been a strictly cash-only enterprise for most of its history and for fairly obvious reasons. Any paper trail would quickly lead to the seller faster than Hansel and Gretel dropped cookie crumbs to find their way home. This cash-only factor has led to many robberies and injuries. But because of the legalization for medical purposes, legal dealers will be able to do many more cashless transactions, significantly reducing its in-person danger.

Because the banking community is one of the most conservative of all financial entities to embrace radical change, it is thought that it will be slow in embracing working capital loans to cannabusinesses, even if it is only for medical purposes. As a result, the loan field is wide open for respected and well-funded companies to meet the burgeoning demand for medical marijuana start-ups in the next 24-36 months.

Working capital loans from non-traditional sources that are not opposed to funding a medical use only marijuana supplier could be used for a number of purposes. Equipment to transport, advertising among a myriad of platforms, and display equipment could be among the reasons for a non-traditional capital loan. In many cases, such a loan would not require a tax return as part of the loan paperwork. And if a supplier can show that it has already been in business for six months or more, First Capital Business Finance can provide loans not only for equipment but for needs such as staff, inventory, and other needs that are not directly tied to physical equipment.

If you are interested in getting into the exploding world of medical marijuana provider services, you will want to talk to the folks at First Capital Business Finance. We have a number of very attractive reasons why our approach to business loans may be right for your new cannabusiness.

Consider these very non-traditional approaches to loan approval:

- Approvals are very fast in being processed, typically within 24 to 48 hours

- Limited paperwork, application & 6 months bank statements are all we need

- As mentioned earlier, most loans do not require a tax return

- If you as the business owner have struggled with credit issues, First Capital Business has an understanding approach to such situations

- Loans can be crafted from 3 to 24 months in length

- Capital loans are available after as little as 6 months in business